TL;DR:

- Estate planning involves organizing your assets, healthcare, and incapacity arrangements to protect your wishes during your lifetime and after your death. It includes essential documents like wills, lasting power of attorney, healthcare directives, and trusts to ensure legal clarity and minimize family disputes. Starting with basic, legally valid plans and updating them regularly helps safeguard your loved ones without delay or unnecessary complexity.

Estate planning is the legal process of arranging how your assets, finances, and healthcare decisions will be managed, both during your lifetime and after your death. Most people assume it is purely about writing a will and deciding who inherits the house. In reality, what is estate planning covers far more than that. It protects you if you become seriously ill, prevents family disputes, and gives your loved ones clear instructions at a time when they need certainty most. This guide explains the estate planning definition in plain terms, walks through the key documents involved, and shows you exactly how to get started.

Table of Contents

- Key takeaways

- What estate planning actually means

- Why estate planning matters beyond inheritance

- The estate planning process: steps for beginners

- Common misconceptions to avoid

- Estate planning is for every adult in the UK

- My perspective on why people delay

- Start your estate plan with Clearlegacy

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Estate planning is broader than a will | It covers asset distribution, incapacity planning, and healthcare decisions during your lifetime. |

| Core documents matter | A will, lasting power of attorney, and healthcare directive each serve a distinct legal purpose. |

| Most adults remain unprepared | Only 24% of adults have a will, leaving the majority legally exposed. |

| Early action beats perfection | Starting with a basic, legally valid will is more protective than waiting until every detail is settled. |

| Regular reviews are non-negotiable | Life changes such as marriage, children, or new property require you to update your plan accordingly. |

What estate planning actually means

The estate planning definition, at its most precise, is the legal process of arranging your affairs so that your wishes are carried out if you die or lose mental capacity. In the UK context, that process sits within a framework of legislation including the Wills Act 1837, the Administration of Estates Act 1925, and the Inheritance (Provision for Family and Dependants) Act 1975.

An estate plan is not a single document. It is a collection of legally binding instruments that together cover the full range of decisions your family may face. The core documents are:

- Last Will and Testament. Sets out who inherits your assets, names an executor to administer the estate, and appoints guardians for any minor children. Under section 9 of the Wills Act 1837, a will must be signed in the presence of two independent witnesses to be legally valid.

- Lasting Power of Attorney (LPA). Authorises a trusted person to manage your finances or make healthcare decisions on your behalf if you lose mental capacity. There are two types in England and Wales: property and financial affairs, and health and welfare.

- Healthcare directive or advance decision. Sometimes called a living will, this document records your wishes about specific medical treatments you do or do not want if you cannot communicate them yourself.

- Trust arrangements. A trust holds assets on behalf of named beneficiaries and can help manage inheritance tax, protect assets for children, or avoid probate delays.

The distinction between a will and a broader estate plan is worth holding clearly in mind. A will only takes effect on death. An estate plan, by contrast, is active throughout your life, shielding you during periods of illness or incapacity as much as it protects your family after you are gone.

| Document | When it applies | Primary purpose |

|---|---|---|

| Will | After death | Asset distribution and executor appointment |

| Lasting Power of Attorney | During life, on incapacity | Financial and healthcare decision-making |

| Advance decision | During life, on incapacity | Specific medical treatment preferences |

| Trust | During life and after death | Asset protection, tax planning, probate avoidance |

Why estate planning matters beyond inheritance

The importance of estate planning is frequently underestimated because most people associate it only with death and inheritance. That framing misses the point. A well-structured estate plan protects you while you are alive just as much as it protects your family once you are gone.

Consider what happens if you suffer a stroke or serious accident and cannot manage your finances or communicate your medical wishes. Without a registered Lasting Power of Attorney in place, your family has no legal authority to act on your behalf. They may need to apply to the Court of Protection, a process that is slow, expensive, and deeply stressful during an already difficult time. An LPA, prepared in advance and registered with the Office of the Public Guardian, prevents that situation entirely.

Beyond incapacity, estate planning serves several other practical purposes.

- Preventing family disputes. Clear written instructions remove ambiguity. Without a will, intestacy rules under the Administration of Estates Act 1925 decide who inherits, which may not reflect your wishes and can cause lasting conflict between relatives.

- Protecting unmarried partners. There is no such thing as common law marriage in England and Wales. An unmarried partner has no automatic right to inherit under intestacy, regardless of how long you have been together. A will is the only legal protection available.

- Managing inheritance tax. The current nil-rate band sits at £325,000, with a residence nil-rate band of £175,000 available when passing a family home to direct descendants. Proper planning can make use of both thresholds and reduce the tax burden on your estate.

- Privacy. A will becomes a public document once probate is granted. A trust arrangement, properly structured, can keep asset distribution private.

Pro Tip: Review your beneficiary designations on pensions and life insurance policies separately. Beneficiary designations override wills, so an out-of-date nomination on a pension can direct money to the wrong person regardless of what your will says.

The low uptake of wills among UK adults means the majority of families are exposed to these risks right now. Getting a plan in place is not morbid. It is one of the most practical things you can do for the people you care about.

The estate planning process: steps for beginners

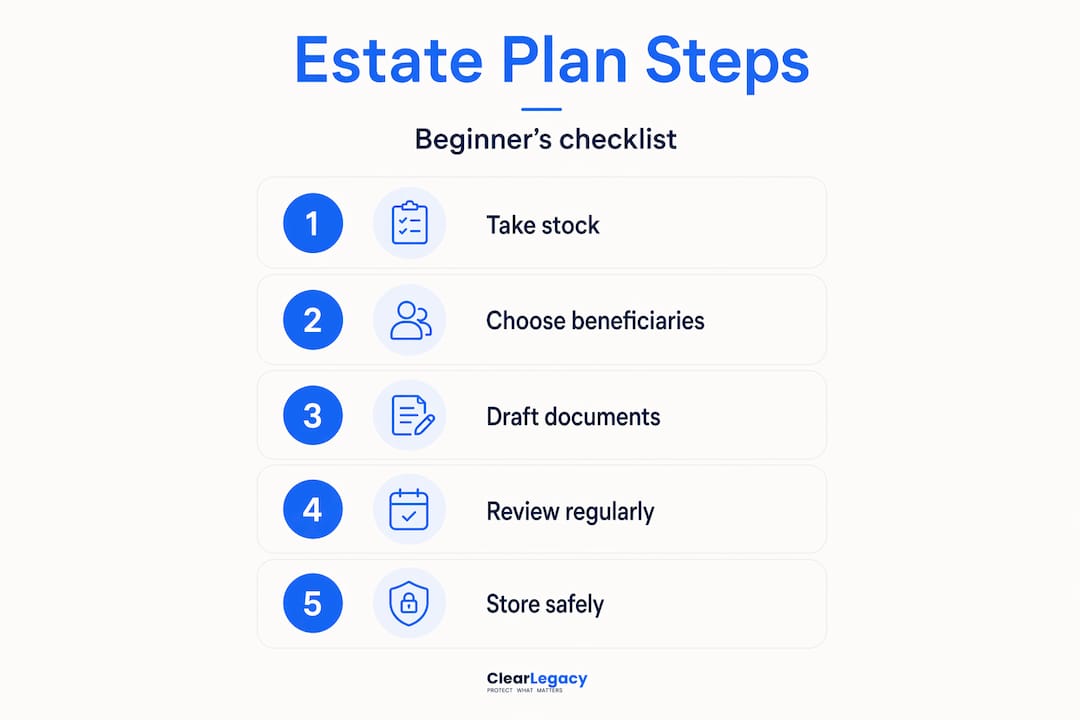

Estate planning for beginners can feel daunting, but the process becomes manageable when you break it into clear stages. These are the five key steps that make up a solid foundation.

-

Take stock of your assets and liabilities. List everything you own: property, savings accounts, investments, pensions, life insurance policies, vehicles, and personal possessions of value. Then list your debts, including mortgages and loans. This inventory tells you what your estate actually comprises and makes it far easier to give clear instructions.

-

Choose your fiduciaries. A fiduciary is someone you appoint to act on your behalf. Your executor carries out your will. A trustee manages any trust you create. Your attorney under an LPA makes decisions if you lose capacity. Choose people you trust completely, and always name a backup in case your first choice cannot act. Naming backup agents is a step many people skip, but it matters significantly if your primary choice predeceases you or loses their own capacity.

-

Draft your core legal documents. At minimum, this means a valid will and a Lasting Power of Attorney for both property and health. If you have children under 18, your will should name a guardian. If inheritance tax planning is relevant, speak to a qualified estate planner about whether a trust is appropriate for your situation. You can get started with writing your will online without the cost and delay of a traditional solicitor appointment.

-

Fund any trusts correctly. Creating a trust document is only half the task. Assets must actually be transferred into the trust by retitling them in the trust's name. Improper trust funding is one of the most common reasons estate plans fail to achieve probate avoidance, even when the documents themselves are well drafted.

-

Review and update your plan regularly. An estate plan is not a one-time task. Marriage, divorce, the birth of children, significant changes in assets, or new legislation can all affect whether your existing plan still does what you intend. A good rule of thumb is to review your plan every three to five years, or immediately after any major life event. Effective estate plans treat this as an ongoing process, not a box ticked once and forgotten.

Pro Tip: If you own property jointly, check whether you hold it as joint tenants or tenants in common. Joint tenants pass the property automatically to the survivor outside the will. Tenants in common can leave their share to anyone they choose. The distinction has significant implications for inheritance tax planning and for protecting your share of the property for children from a previous relationship.

Common misconceptions to avoid

Several widely held beliefs about estate planning lead people to think they are protected when they are not.

- "My will covers everything." A will does not govern assets held in trust, pensions, jointly held property passing by survivorship, or any account with a named beneficiary. These pass outside the will entirely, which is why a broader estate plan is necessary.

- "I do not need a power of attorney while I am healthy." An LPA must be registered before it is needed. You cannot create one after you have lost mental capacity. Waiting until a health crisis strikes is too late.

- "DIY documents are fine for simple estates." Straightforward circumstances can quickly become complicated by blended families, overseas assets, or business interests. DIY and AI-generated estate plans often fail to address these nuances and risk not meeting the legal formalities required under the Wills Act 1837. A plan that fails on a technicality offers no protection at all.

- "Estate planning is for the wealthy." The statutory legacy under intestacy rules stands at £322,000 (from July 2023). Anyone with assets, a home, or children above that threshold who dies without a will leaves their family navigating a complicated legal process at an already painful time.

Reviewing your estate planning options does not require significant time or cost. What it does require is taking that first step.

Estate planning is for every adult in the UK

There is a persistent assumption that estate planning is something you do when you are older, wealthier, or at some better-defined point in the future. None of those criteria are relevant. If you have a partner, children, a home, or any savings at all, you have an estate worth planning.

The Inheritance (Provision for Family and Dependants) Act 1975 gives certain family members and dependants the right to make a claim against an estate if they feel inadequately provided for. A clearly drafted will with well-reasoned provisions reduces the likelihood of a successful challenge significantly.

Peace of mind is not an abstract benefit. Knowing that your family will not face avoidable legal costs, delays, or disputes if something happens to you is genuinely valuable. A legally valid will, a registered Lasting Power of Attorney, and a clear advance decision can turn the worst day in a family's life from a legal disaster into a manageable administrative process.

My perspective on why people delay

In my experience, the single biggest barrier to estate planning is not cost or complexity. It is the search for the perfect moment. People wait until after the house purchase completes, until after the new baby arrives, until life feels more settled. That moment rarely comes.

Procrastination driven by analysis paralysis is the real threat to your family's security, not the lack of a perfectly structured plan. I have seen families struggle through intestacy proceedings that could have been avoided entirely by an afternoon's worth of preparation. A basic, legally valid will and a registered LPA do more good than a theoretically perfect plan that never gets written.

My advice is simple: do the core documents now, and refine later. Life changes, and your plan should change with it. But an imperfect plan that exists protects your family. A perfect plan that remains unwritten protects nobody.

— Sat

Start your estate plan with Clearlegacy

If this article has clarified what estate planning involves and why it matters, the logical next step is to put that understanding into action.

Clearlegacy offers a straightforward online will writing service starting at £69, with a fixed price and no hidden fees. You can complete your will in around 15 minutes, and receive a legally valid document by email within 24 hours. Every will is prepared using a guided digital process and reviewed by a qualified estate planner, so you get the speed of an online service without sacrificing legal compliance under the Wills Act 1837. If you want to understand your options before committing, the UK online will comparison guide on the Clearlegacy website sets out exactly what to look for. Over 100 UK families have already used Clearlegacy to protect their legacies. Yours can be next.

FAQ

What does estate planning include in the UK?

Estate planning in the UK typically includes a Last Will and Testament, a Lasting Power of Attorney (for both financial and health decisions), an advance decision on medical treatment, and trust arrangements where relevant for tax or asset protection purposes.

Do I need estate planning if I have a small estate?

Yes. Anyone with a partner, children, or assets of any value benefits from having a will and a Lasting Power of Attorney in place. Without a will, intestacy rules under the Administration of Estates Act 1925 determine who inherits, which may not reflect your wishes.

How often should I update my estate plan?

You should review your estate plan every three to five years and immediately after major life events such as marriage, divorce, the birth of a child, or a significant change in assets. Regular reviews keep the plan aligned with your current circumstances and any changes in legislation.

Can an unmarried partner inherit without a will?

No. There is no common law marriage in England and Wales. An unmarried partner has no automatic right to inherit under intestacy rules, regardless of the length of the relationship. A valid will is the only way to protect an unmarried partner's inheritance rights.

Is an online will legally valid in the UK?

Yes, provided it meets the requirements of section 9 of the Wills Act 1837: it must be in writing, signed by the testator, and witnessed by two independent adults who are present at the same time. Clearlegacy's wills meet these requirements and are reviewed by qualified estate planners before delivery.