TL;DR:

- Regular review of estate plans is essential to ensure they remain legally effective and reflective of current circumstances. Neglecting professional reviews can lead to probate delays, unintended tax liabilities, and family disputes, jeopardizing your wishes. Engaging qualified estate planners and incorporating periodic updates safeguard your estate, offering peace of mind and legal certainty.

Most people write a will, file it away, and assume their estate is sorted. It is not. The role of estate planner review is to catch everything that shifts between that moment and the one that matters most: when your family needs your plan to actually work. Laws change, assets move, families grow and fracture, and a document drafted five years ago may no longer reflect your wishes or comply with current legislation. This article explains what a professional estate planning review involves, why skipping it carries real financial and legal risk, and how to approach the process confidently.

Table of Contents

- Key takeaways

- The role of estate planner review in the planning process

- What gets checked during an estate planner review

- Risks of skipping a professional review

- How to review your estate plan and choose a planner

- Online services, solicitors, and estate planners compared

- My honest view on why reviews get neglected

- Start your estate plan review with Clearlegacy

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Reviews are not optional extras | Estate plans should be reviewed every 3 to 5 years or after major life events to remain legally effective. |

| Professional oversight prevents failure | Asset re-titling, beneficiary updates, and tax compliance are all checked during a thorough estate planner review. |

| Outdated plans cost families dearly | Probate delays and unintended tax liabilities are common consequences of plans that have not been professionally reviewed. |

| Qualifications matter when choosing a planner | Look for verifiable credentials, ongoing professional development, and experience with UK-specific legislation. |

| Online services can work alongside reviews | Accessible platforms like Clearlegacy pair digital convenience with qualified planner oversight for a legally sound result. |

The role of estate planner review in the planning process

An estate planner does far more than draft a will and hand it over. Their role spans the entire lifecycle of your estate plan, from the initial assessment of your assets, family structure, and wishes, through to the periodic reviews that keep everything aligned with your current life and the law.

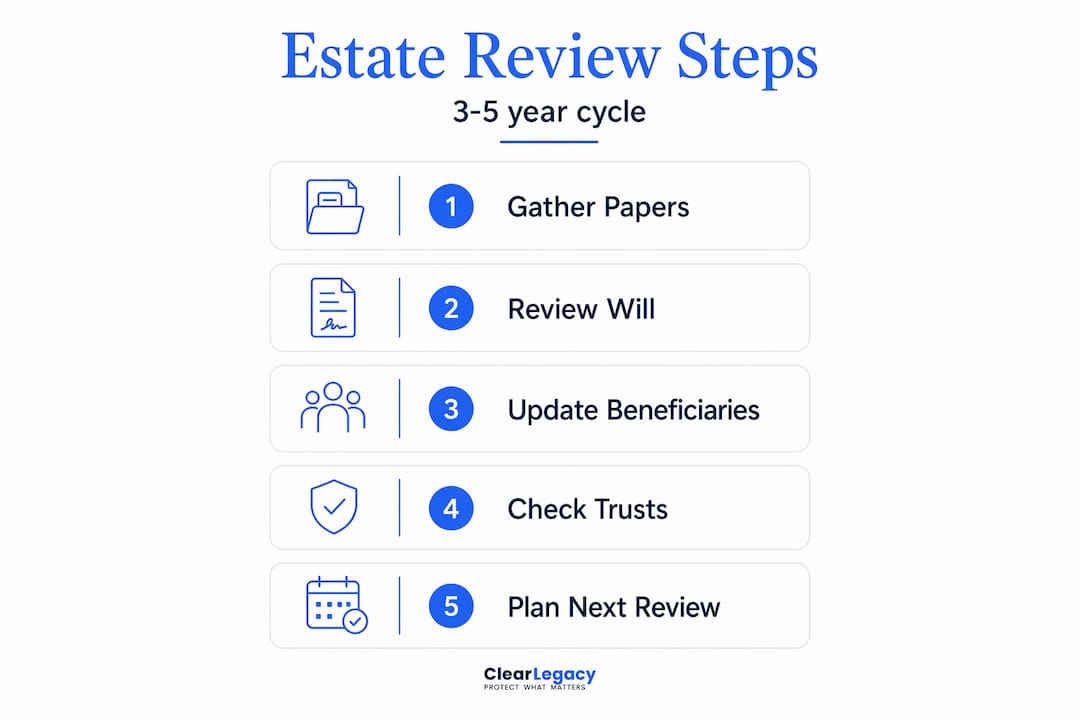

Estate plans are not one-time documents; they require revisiting every 3 to 5 years or after any significant change in your circumstances. A qualified estate planner brings continuity to this process. They hold the history of your planning decisions and can identify what has shifted since the last review, whether that is a change to HMRC's inheritance tax thresholds, a new grandchild, the purchase of a second property, or a relationship breakdown.

It is worth understanding a distinction that often causes confusion. Consumers frequently confuse estate planners with estate solicitors; only solicitors and qualified legal professionals can draft legally binding documents in England and Wales. Estate planners, in the broader sense, may coordinate the process, advise on structure, and manage the review, but the legal drafting must meet the requirements of section 9 of the Wills Act 1837 to be enforceable.

The review process is what transforms a static document into a living plan. Without it, your will may still be technically valid, yet completely misaligned with who you are now, what you own, and what you want.

Pro Tip: Set a recurring calendar reminder every three years to prompt a review. Major life events should trigger an immediate check rather than waiting for the scheduled interval.

What gets checked during an estate planner review

A thorough review covers considerably more than reading through your existing will and confirming the executors are still willing to act. It is a structured examination of your entire estate planning picture, touching on several interconnected areas.

-

Wills and testamentary documents. Your will is checked for internal consistency, clarity of instruction, and compliance with current law. Any residuary clause or specific bequest that may now create ambiguity is flagged and revised.

-

Trusts and their funding status. Re-titling assets into a trust is often overlooked, meaning the trust exists on paper but holds nothing. A review confirms that the trust is properly funded and that any new assets acquired since the last review have been correctly transferred.

-

Lasting Powers of Attorney. Your property and financial affairs LPA, as well as your health and welfare LPA, are reviewed for current relevance. If an appointed attorney has died, lost capacity, or your relationship with them has changed, the documents must be updated.

-

Beneficiary designations. Pensions, life insurance policies, and certain investment accounts pass outside of your will. If beneficiary designations have not been updated to reflect family changes, assets can pass to an ex-spouse or a deceased person, bypassing your current wishes entirely.

-

Inheritance tax position. The review checks your exposure against current HMRC thresholds, the £325,000 nil-rate band and the £175,000 residence nil-rate band, and identifies whether any planning opportunities such as gifts, charitable legacies, or trust structures could reduce your family's liability.

-

Co-ordination with financial and tax advisers. Lack of communication between estate planners and tax advisers can trigger unintended tax liabilities. A good review process brings these professionals into alignment so nothing falls through the gap.

Pro Tip: Before your review appointment, gather your most recent mortgage statement, pension paperwork, insurance schedules, and any trust deeds. Your planner can only review what they can see.

Risks of skipping a professional review

The consequences of an unreviewed estate plan are not abstract. They are financial, legal, and deeply personal.

-

Probate delays and costs. Probate fees can consume up to 5% of estate value and the process can take well over a year when documents are unclear or disputed. An outdated will that names an executor who has since died, or refers to a property that was sold, can significantly extend that timeline.

-

Unintended tax liabilities. Tax legislation changes frequently. Nil-rate band thresholds, exemptions, and reliefs available to your estate in 2019 may not apply in the same way today. Without a review, your family may face an inheritance tax bill that careful planning could have reduced.

-

Plan failure from unfunded structures. A trust that holds no assets provides no protection. Reviews ensure documents reflect current family and financial situations, confirming that the legal structures created actually contain the assets intended.

-

Family conflict and legal challenges. Ambiguous or outdated wills are among the most common causes of contested estates under the Inheritance (Provision for Family and Dependants) Act 1975. Disputes over what a testator intended are painful, expensive, and often avoidable.

-

False security from DIY or unreviewed plans. A will written using an online template and never professionally reviewed may be signed correctly yet still fail in ways the drafter did not anticipate.

"Estate planning is not simply avoiding probate but managing estate administration effectively to reduce beneficiary distress and executor load." Kitces Financial Planning

How to review your estate plan and choose a planner

Timing and preparation make the difference between a review that genuinely protects your family and one that merely confirms paperwork is in order.

When to seek a review

Certain life events should prompt an immediate review, regardless of when you last had one:

- Marriage or entering a civil partnership (a new marriage revokes a previous will in England and Wales)

- Divorce or separation

- Birth or adoption of a child or grandchild

- Significant change in assets, such as inheriting property or selling a business

- Death or incapacity of an executor, attorney, or named beneficiary

- Moving abroad or acquiring overseas assets

- Changes to inheritance tax legislation

Beyond these triggers, a review every three to five years as a baseline keeps your plan current without becoming burdensome.

Questions to ask your planner during a review

Arriving with clear questions makes the session more productive:

- Does my current will reflect my wishes accurately, including any new assets or relationships?

- Are all my trusts properly funded and legally current?

- What is my current inheritance tax exposure, and what planning options exist?

- Are my LPAs still fit for purpose?

- How does my pension nomination align with my wider estate plan?

Choosing a qualified estate planner

In the UK, look for a solicitor regulated by the Solicitors Regulation Authority, a member of the Society of Trust and Estate Practitioners (STEP), or a specialist will writer who is a member of the Institute of Professional Will Writers. Avoid any provider who cannot demonstrate ongoing professional development. Accredited Estate Planner designees must complete 30 hours of continuing education every 24 months, and equivalent standards should be your benchmark when choosing a UK professional.

| What to look for | What to avoid |

|---|---|

| SRA-regulated solicitor or STEP member | Unregulated will writers with no professional body membership |

| Fixed-fee or clearly disclosed pricing | Open-ended or unclear fee structures |

| Experience with blended families or complex assets | Generalist advisers with no estate planning specialism |

| Co-ordination with your tax adviser | Planners who work in isolation from your financial picture |

| Willingness to review and update, not just draft | One-off document providers with no ongoing relationship |

Online services, solicitors, and estate planners compared

Understanding the differences between service types helps you know what you are getting and what you may be missing.

A solicitor is the gold standard for complex estates: blended families, business interests, significant assets, or contentious family circumstances. They can draft legally binding documents, advise on tax, and represent your estate in the event of a dispute.

A specialist estate planner or will writer regulated through STEP or the IPW can handle the majority of straightforward and moderately complex situations competently and often at lower cost than a full solicitor engagement.

Online will services vary considerably in quality. DIY estate planning tools often lack legal nuance; professional reviews reduce the risk of litigation and address enforceability problems that template documents cannot anticipate. The key question is whether the service includes qualified review or simply automates document production.

Clearlegacy sits in a distinct position here. Its AI-assisted platform prepares documents which are then reviewed by qualified estate planners, meaning you benefit from digital speed without sacrificing the professional oversight that makes a will legally sound and practically effective. You can explore the pros and cons of online wills and read a detailed online will vs solicitor comparison to decide which route suits your circumstances.

For most straightforward estates, the combination of a professional online platform with qualified review offers a genuinely good outcome. For complex situations, that review may identify the moment to involve a full solicitor.

My honest view on why reviews get neglected

I have seen the same pattern repeat itself. A couple writes their wills after the birth of their first child, relieved to have it done, and then life accelerates. A second child, a house move, an inheritance from a parent, a business started at the kitchen table. Twenty years pass. The will still names an executor who emigrated in 2014 and leaves everything to a spouse under an assumption of intestacy rules that may not operate as expected.

What strikes me is that the neglect is almost never intentional. Analysis paralysis delays clients from seeking reviews; the relationship built over time with a trusted planner is what ultimately produces an estate plan that holds together. People know the plan probably needs updating. They just do not know where to start, and the discomfort of thinking about death and money together is enough to push the task indefinitely onto tomorrow's list.

The other thing I have observed is that the one-off document mindset is genuinely costly. Families who maintain an ongoing relationship with a qualified planner, who treat the review as a routine part of managing their affairs rather than an uncomfortable errand, almost always end up in a better position. Not because their plans are dramatically more sophisticated, but because small corrections made regularly prevent large problems later. The value of the review is not usually one big dramatic intervention. It is dozens of small adjustments that collectively mean everything works when it needs to.

If you have not reviewed your estate plan in the last three years, that is the starting point. Not a full overhaul. Just a conversation.

— Sat

Start your estate plan review with Clearlegacy

If this article has prompted you to take stock of where your estate plan currently stands, the next step does not have to be complicated or expensive. Clearlegacy's will writing service starts from just £69 and combines a fast, user-friendly digital process with review by qualified estate planners, meaning your document is checked for legal compliance under the Wills Act 1837 before it reaches you.

Whether you are writing a will for the first time or updating an existing one, Clearlegacy delivers a legally valid document within 24 hours, with fixed pricing and no hidden fees. Over 100 UK families have already used the service to protect what matters most. If you want to write your will online today and receive it by tomorrow, Clearlegacy makes that straightforward.

FAQ

How often should an estate plan be reviewed?

Estate plans should be reviewed every 3 to 5 years as a minimum, and immediately after major life events such as marriage, divorce, birth of a child, or a significant change in assets.

What does an estate planner review actually cover?

A professional review checks your will, any trusts and their funding status, Lasting Powers of Attorney, beneficiary designations on pensions and life policies, and your current inheritance tax position against HMRC thresholds.

Is it safe to use an online will service without a professional review?

Without professional review, online wills carry legal risks that template automation cannot resolve, including enforceability problems and gaps in document co-ordination. Services that include qualified planner review, like Clearlegacy, significantly reduce this risk.

What qualifications should I look for in a UK estate planner?

Look for a solicitor regulated by the Solicitors Regulation Authority, or a specialist regulated through STEP (Society of Trust and Estate Practitioners) or the Institute of Professional Will Writers. Ongoing professional development is a reliable indicator of a planner who keeps pace with legal changes.

Can an unreviewed estate plan lead to probate problems?

Yes. Outdated or ambiguous documents are a leading cause of probate delays; probate costs can reach up to 5% of estate value and the process frequently takes well over a year when documents are contested or unclear.