TL;DR:

- Joint estate planning involves coordinating wills, asset ownership, and beneficiary designations to reflect shared intentions.

- Proper planning prevents conflicts caused by asset titling and legal discrepancies, ensuring your wishes are upheld.

Many couples assume that signing a single document together is all joint estate planning involves. It is not. Joint estate planning explained properly means understanding how your wills, asset ownership, beneficiary designations, and property titles all work together as one coherent plan. Done well, it can turn the worst day in a family's life from a legal disaster into a straightforward paperwork exercise. Done poorly, even a carefully written will can be undermined by how your bank account or property is titled. This guide covers everything you need to know, from joint wills to mirror wills, ownership structures, and practical steps for keeping your plan current.

Table of Contents

- Key takeaways

- What is joint estate planning?

- Joint wills versus mirror and mutual wills

- Asset ownership, titling, and non-probate transfers

- Best practices for joint estate planning

- My perspective on where couples go wrong

- Start your joint estate plan with Clearlegacy

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Joint wills are one document | A joint will is signed by two people but may be difficult to change after the first death. |

| Mirror wills offer more flexibility | Separate but coordinated wills are favoured by most modern couples for their adaptability. |

| Asset titling overrides your will | How property and accounts are titled determines how they transfer, regardless of what your will says. |

| Regular reviews are non-negotiable | Major life events require updates to wills, beneficiary designations, and property titles. |

| Professional coordination matters | Aligning all documents and registrations prevents costly conflicts during estate administration. |

What is joint estate planning?

Joint estate planning is the process by which two people, typically a married couple or cohabiting partners, coordinate their wills, asset ownership structures, and beneficiary designations to reflect shared intentions. The recognised industry term for the formal document at its centre is a joint will, though the broader planning process encompasses far more than a single document.

A joint will is one document signed by two people that sets out how their combined assets will be distributed after both have passed away. It is executed under the same formalities as any individual will: signed in writing, signed by the testators, and witnessed by two independent witnesses present at the same time, as required under section 9 of the Wills Act 1837.

Typical provisions in a joint will include:

- The surviving spouse or partner inherits the estate in full on the first death.

- After both deaths, the remaining estate passes to named beneficiaries, often children.

- A residuary clause handles any assets not specifically mentioned.

- Guardians for minor children may be appointed within the same document.

The document functions like a contract between two people about the future of their shared estate. However, a critical and widely misunderstood point is whether it is binding. Joint wills are not automatically binding on the surviving partner. Unless there is clear evidence of a separate binding agreement (known in law as a mutual will agreement), the surviving spouse can legally revoke or alter the will after the first death.

Pro Tip: Never assume a joint will locks your surviving partner into your shared wishes. If binding succession is what you need, you must enter into a formal mutual wills agreement with separate legal advice. Speak to a qualified estate planner before proceeding.

Joint wills versus mirror and mutual wills

Understanding what is joint estate planning means knowing the differences between three distinct approaches. Each carries different legal weight, different flexibility, and different risks.

| Will type | Structure | Binding? | Flexibility | Best suited to |

|---|---|---|---|---|

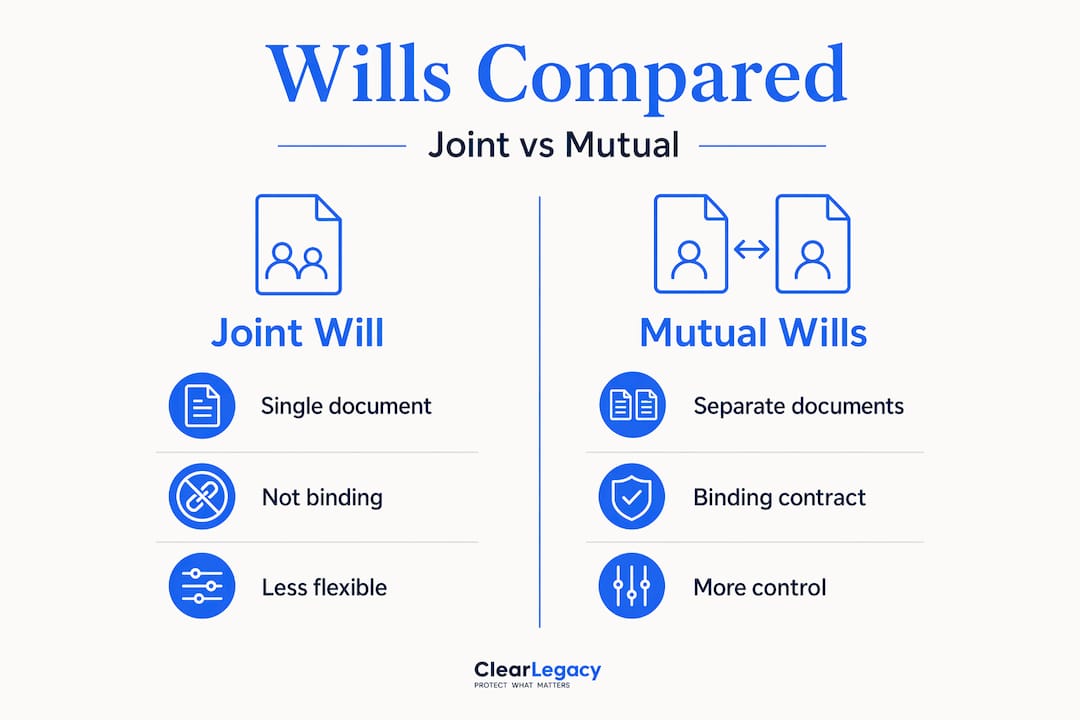

| Joint will | One document, two testators | Not automatically | Low after first death | Simple estates, no anticipated changes |

| Mirror wills | Two separate, coordinated documents | No | High; each can be changed independently | Most couples, standard estates |

| Mutual wills | Two documents with a binding agreement | Yes, by contract | Very low; survivor cannot change without breach | Complex estates, blended families wanting certainty |

Mirror wills are separate but similar documents that allow each partner to leave their estate to the other, then to shared beneficiaries. Crucially, each person can update their own will independently after the other has died. This makes mirror wills the preferred option in modern practice for most couples, including those with children from previous relationships or evolving financial circumstances. You can learn more about your options as an unmarried couple in Clearlegacy's guide to wills for unmarried couples.

Mutual wills go further. They involve a binding contract not to revoke or alter the wills after the first death. The risk of joint wills and mutual wills alike is their inflexibility. If your circumstances change after the first death, whether through remarriage, new children, or significant changes in your financial position, you may be legally prevented from reflecting those changes.

For blended families, where children from previous relationships have competing claims, a solicitor-drafted mutual wills arrangement with clear trust provisions is often more appropriate than either a joint or a standard mirror will.

Pro Tip: If you have children from a previous relationship, do not rely on your partner's goodwill to honour your wishes after you die. A trust embedded in mirror wills, or a properly drafted mutual wills agreement, gives your children legal protection without requiring a contested court action.

Asset ownership, titling, and non-probate transfers

Here is the part of joint estate planning that catches most couples off guard. Your will only controls assets that pass through your estate. Many assets do not pass through your estate at all. Non-probate mechanisms such as joint tenancy, beneficiary designations, and registered contracts control the transfer of a large proportion of most families' wealth, entirely independently of any will.

The two most common property ownership structures in England and Wales are:

| Ownership type | How it works | Probate required? | Can will override it? |

|---|---|---|---|

| Joint tenancy | Both owners hold equal shares; survivor inherits automatically | No | No |

| Tenants in common | Each owner holds a defined share (can be unequal) | Yes, for deceased's share | Yes |

Joint tenancy transfers property automatically to the surviving owner by operation of law, bypassing probate and overriding anything your will says about that property. If your will leaves your half of the family home to your children but you hold it as joint tenants with your partner, your children receive nothing from that asset. Careless titling can effectively write out intended heirs without anyone realising until it is too late.

Tenants in common, by contrast, lets each partner own a distinct share. Your share forms part of your estate on death and can be directed by your will to whomever you choose. This structure is particularly valuable for:

- Couples where one partner has children from a previous relationship.

- Situations where protecting an individual's share for a specific beneficiary matters.

- Estates where one partner contributed significantly more to the purchase price.

Ownership type determines how assets transfer at death, making an accurate asset inventory the foundation of any reliable joint estate plan. For guidance on how to include property correctly in your will, Clearlegacy's property and wills guide is a practical starting point.

Best practices for joint estate planning

The shared estate planning process explained clearly comes down to one principle: every part of your plan must point in the same direction. A will that says one thing while your bank account or property title says another creates confusion, delays, and sometimes litigation. Couples should align titles, beneficiary designations, and estate documents to prevent precisely these conflicts.

These are the practices that make the difference between a plan that holds and one that falls apart:

- Create a full asset inventory. List every asset, including property, savings accounts, pensions, investments, and life insurance. For each one, note the current ownership structure and how it will transfer on death.

- Review beneficiary designations separately. Pension schemes and life insurance policies pass outside your estate. The beneficiary named on those forms takes precedence over your will. Check them every few years and after every major life event.

- Align your documents. Your will, any trusts, your property title, and your beneficiary nominations should reflect the same wishes. Mismatches between asset titling and testamentary documents are the most common cause of unintended distributions.

- Update after major life events. Marriage, divorce, the birth of a child, a significant inheritance, or the purchase of property are all triggers to review your entire plan, not just your will.

- Take professional advice for complexity. Blended families, business interests, properties held in trust, or estates above the £325,000 nil-rate band require specialist input to manage inheritance tax exposure and succession correctly.

Gathering documentation for non-probate assets can take weeks to months, so leaving your estate in good order is a practical gift to the people who will administer it. Clear records of where everything is held, and how it is owned, reduce the burden considerably.

Pro Tip: Keep a single secure document, updated annually, that lists all your assets, their ownership structure, and where the relevant account or title documents are held. Store it alongside your will. This alone can save your family weeks of administration.

My perspective on where couples go wrong

What I have observed consistently is that couples treat the signing of a will as the finish line. It is not. It is closer to the starting point.

The most avoidable problems I see arise not from bad wills, but from good wills sitting alongside incompatible asset titles. A couple carefully writes mirror wills leaving everything to each other, then to their children. They feel sorted. What they have not noticed is that their savings account is in joint names with a right of survivorship, their life insurance policy still names an ex-partner, and their property is held as joint tenants when tenants in common would better protect their children's inheritance.

The will says one thing. The rest of the estate says something different. When one of them dies, the will is almost irrelevant for the bulk of their assets.

The other pattern I see is the reluctance to revisit plans after life changes. A will written before a second marriage, the arrival of a stepchild, or a significant change in wealth can produce outcomes that bear no resemblance to what either partner would have wanted. Flexibility is not a sign of indecision. It is a sign of good planning.

My honest advice: do the asset inventory before you write the will. And review both together every three to five years, not just when something goes wrong.

— Sat

Start your joint estate plan with Clearlegacy

If this guide has clarified one thing, let it be this: joint estate planning is not complicated, but it does need to be done properly. The good news is that it does not need to be expensive or time-consuming.

Clearlegacy provides a straightforward online will writing service starting from just £69, designed specifically for UK families who want legally valid, professionally reviewed wills without the cost of lengthy solicitor appointments. Couples can create coordinated mirror wills that reflect shared wishes while keeping each partner's document independent and updatable. Every will is reviewed by a qualified estate planner and complies fully with the Wills Act 1837. You can complete your will in around 15 minutes and receive it by email within 24 hours. Over 100 UK families have already used Clearlegacy to protect what matters most. If you are ready to take the first practical step, write your will online today.

FAQ

What is a joint will in the UK?

A joint will is a single legal document signed by two people, usually spouses or partners, that sets out how their combined assets will be distributed after both deaths. It must comply with the formalities of the Wills Act 1837.

Are joint wills legally binding in England and Wales?

A joint will is not automatically binding on the surviving partner. Unless a separate mutual wills agreement with clear evidence of intent exists, the survivor can revoke or alter the will after the first death.

What is the difference between joint wills and mirror wills?

Mirror wills are two separate but coordinated documents, each independently revocable, whereas a joint will is a single document shared by both partners. Most UK couples choose mirror wills for their greater flexibility.

Can asset ownership override my will?

Yes. Assets held in joint tenancy pass automatically to the surviving owner outside probate, regardless of what your will instructs. Beneficiary designations on pensions and life insurance policies work the same way.

How often should couples review their joint estate plan?

Every three to five years as a minimum, and after any major life event such as marriage, divorce, the birth of a child, or a significant change in assets or property ownership.